Welcome back to the Great North Ventures newsletter! This month we have advice for founders featured in our latest podcast episode.

In the latest episode of “Execution is King” we feature the best advice for founders, recorded live at our 2021 Annual Event.

What is the Great North Annual Event? Every year, we gather investors, founders, and ecosystem builders together for networking and progress updates.

This year, we captured advice from our stakeholders, people who have proven they can execute.

Listen to the full episode for guidance on:

- Hiring and Firing

- Leadership

- Go to market

…and more.

Two ventures from our venture studio, NextGem and Backhouse Brands, are hiring. If you are interested in getting in early with a high-growth startup opportunity, check out these open positions.

- Backhouse Brands is hiring a Head of Sales based in St.Cloud or Remote.

- NextGem is hiring a Lead Mobile Product Designer and a Lead Software Engineer in Grand Rapids, Minneapolis, or Remote.

Portfolio Updates

Flywheel Partners with Roche and Genentech to Accelerate

Development of Personalized Healthcare Solutions

vWise partners with IRALOGIX to enable rapid deployment of IRA solutions

Outstate MN: Innovation in Central Minnesota [ZenLord Pro]

Hot 25 Startups 2022: NoiseAware

105 Open Positions

See all open positions on the Great North Ventures careers page

Dispatch is hiring for 70 positions

FactoryFix is hiring for 6 positions

Parallax is hiring for 2 positions

Branch is hiring for 16 positions

Inhabitr is hiring for 3 positions

NoiseAware is hiring for 2 positions

PartySlate is hiring for 2 positions

Flywheel is hiring for 1 position

NextGem is hiring for 2 positions

Backhouse Brands is hiring for 1 position

Over 10,700 venture-backed companies received a combined $136.5 billion in funding in 2019, and the year saw double the exit value of 2018.[i] As stocks, real estate investments, and venture capital reach record highs, what are investors thinking about where to invest?

The answer depends on the type of investor:

- Large funds such as university endowments, pension funds and funds-of-funds have been allocating a part of their portfolio to venture capital for many years now and have seen success. Universities like the University of Minnesota[ii], Stanford[iii] and Yale[iv] have done very well with venture investments. For the fiscal year ending June 2015, the University of Minnesota invested 26.1% of its capital in private investments, with 14% of the private allocation invested in venture capital. The overall fund returned 5.7%, private capital returned 16.1%, and venture capital returned 28%.[v] This has increased the appetite for venture investments among endowments.

- High net worth individuals who have built their wealth in tech are reinvesting in tech venture funds.

- High net worth individuals who have traditionally invested in the stock market, real estate, or private equity, are warming up to tech venture investing.

- Family offices are increasingly doing the same. In a recent tally of the attendees of a US family office event, 35 out of 60 firms expressed interest in venture capital.

Is this a good time for venture investing?

If the economy continues to do well, venture investments will do well. If the economy falters or if there is a stock market correction, this may still be a good time to invest in venture capital.

This is because stock market corrections (and corrections in the real estate market, which usually follows the stock market) follow business cycles, which can last 4-7 years. Venture funds usually invest over a 9-10 year investment cycle (i.e., a 5-6 year investment period followed by a 4-5 year harvest period). A slower business climate or stock market correction ahead could well be bracketed within the life of a new fund. And if needed, with due approvals from the limited partners, venture funds can extend their term to time their exits better.[vi]

Is there benefit in investing in venture funds in down cycles?

Let us look at the dynamics of different asset classes in downturns.

- Real estate – During the 2008 financial meltdown, real estate crumbled. As people lost their jobs, renters could not pay their rents, and property owners could not cover their mortgages. As defaults grew, real estate prices dropped. The Case-Shiller index dropped from 195 in 2005 to 116 in 2011.[vii] Considering the leverage of real estate investments, the losses for investors were much higher.

- Stocks, ETFs – The stock market similarly took a serious hit. The DJIA dropped 54% from 14,164 to 6,469 over 17 months.

- Venture capital – From Q1 2008 to Q1 2009, venture funding fell by 50% nationally to $3.9 billion (Dow Jones Venture Source).

Why did venture capital fare better than real estate or stocks?

First, lean times promote capital efficiency. As is often heard, recessions are the best time to start new companies, which is where early-stage venture capital is focused.

Second, venture capital firms mark up or mark down their investments over their life cycle. However, as actual valuations are pegged only by liquidity events, the real IRR is not known until the investments achieve liquidity. During the holding period, capital-efficient companies, and venture companies that focus on capital efficiency, do well, i.e., are counter-cyclical. They suffer fewer dislocations during downtimes. They can maintain their strategies, continue to do business as usual, and get ahead of those that slow down. Employees of such companies are more secure and loyal. And if needed, high-quality talent not available during good times can be hired, with loyalty that again pays dividends over the long term.

The capital efficiency of the upper Midwest

Companies in the upper Midwest inherently tend to be capital-efficient because there is less capital available. Similarly, smaller funds such as there are in the upper Midwest are inherently more capital-efficient, as they have less to invest.

44% of venture capital flows into Silicon Valley.[viii] This sets the consumption set-point of Silicon Valley companies at much higher burn rates than in regions where availability of venture funds is limited. The relative lack of available capital in other regions, including the upper Midwest, instills caution in spending.

Employee wages

While most other expenses are comparable across the US, with legendary real estate prices, Silicon Valley employees cannot survive at less than Silicon Valley wages.

This is not true in the upper Midwest. Though other expenses are comparable, housing costs may vary from 1/3rd to 1/10th of the Bay Area, enabling much greater capital efficiency for employers. For example, Google employees can buy 5 houses for the price of one by moving to one of Google’s locations across the country.[ix]

Figure 1. The real estate cost advantage of the upper Midwest compares well against not only the most expensive regions in the US, but also against what may be incorrectly perceived as lower-cost overseas regions (e.g., China). Seven cities in China and an equal number of cities in the US are listed above Minneapolis.

Fold? Hold? Or double down?

Not only can capital-efficient companies continue without disruption during slow times, given the lag between investment and market benefit, those that increase their investment can emerge even stronger in a recovery.

Intel applied this counter-intuitive strategy across many recessionary cycles, and invested several billion dollars in down cycles.[x] When their new semiconductor fabrication capacity resulting from these investments came online a few years later, their timing coincided with market rebound. On the other hand, competition (e.g., Atmel, Fairchild, Intersil/GE, IBM, Motorola, Raytheon, and several others) weakened from retrenchment and lost market share. As the industry consolidated during down cycles, Intel gained market share, and cumulatively over several cycles, emerged as its leader.

Some investors may feel that liquidity is useful during a downtime. Others argue against it, as getting out of the game when entrepreneurs are especially capital-efficient has a higher opportunity cost, and to use the Intel analogy, puts the winners further ahead of the losers. According to a prominent Silicon Valley investor, “you got to stay in the game”. At these times there are opportunities to go one step farther and double down.

Are smaller funds better than larger funds?

The statistical odds of a unicorn (company valued at over $1B) are lower than, say, of a ‘deci-corn’ (company valued at over $100M). Larger funds invest larger amounts per deal. To return high multiples, they need unicorns, which are rare. Smaller funds invest smaller amounts and can get the same multiples from ‘deci-corns’, which are much more common.

Advantages for Midwest venture capital

There are other tactics used by, and attributes common to, small Midwest VC’s that safeguard against downturns:

- Global investments that require skills available in the upper Midwest. While staying abreast of the latest trends in Silicon Valley to stay competitive, Midwest VC’s can take advantage of expertise available in the upper Midwest to serve global markets. In so doing, they avoid the valuation markups and early-round dilutions of Silicon Valley yet seek global parity in later rounds and exits.

- Local investments, global exits. An emphasis on the upper Midwest inherently allows investing at a discount compared to the investments in overheated markets such as Silicon Valley. This roughly translates to a 60% discount in term sheets offered on companies in the Upper Midwest. Global businesses rooted in the upper Midwest still attain exit valuations that correlate with global valuations. Thus, if a down cycle may require 50% markdowns for some Silicon Valley funds, Midwest VC’s can still record a 10% (=60-50%) markup at the bottom of the trough, emerge stronger from uninterrupted progress from investees’ capital efficiency, and exit with a markup brought to parity with global valuations in strong economic times.

- Emphasis on product-market fit. With the reduced capital investment now possible in many tech businesses, the barrier to entry has been lowered. Smaller venture funds can adjust criteria to focus investments on product-market fit, early revenue, and early break-even and profitability, instead of being limited by the number of affordable investment options. Nothing demonstrates product-market fit and staying power than paying customers and profit; for customers, employees and investors alike, there is nothing more powerful than profitability. Judicious investment in such businesses and mentorship to focus teams on profitability facilitates survival in lean times.

- Operators as investors. Small venture funds are often started by former operators with past successful exits, and the Midwest is no different. Many Midwest VC’s have a history of building profitable businesses the old-fashioned way, a dollar at a time. This experience of running a company, of managing payroll through good times and bad, of knowing the revenue and cost management discipline required to make money operationally and sustainably (i.e., not with short-term financial engineering), is invaluable for VC’s to have. So much so, that even accomplished operators will supplement their teams with experienced industry advisors.

[i] https://pitchbook.com/news/reports/q4-2019-pitchbook-nvca-venture-monitor

[ii] https://www.bizjournals.com/twincities/news/2018/03/15/how-the-leader-of-the-university-of-minnesotas.html

[iii] https://www.wsj.com/articles/robert-f-wallace-named-ceo-of-stanfords-endowment-1427138729

[iv] https://news.yale.edu/2017/10/10/investment-return-113-brings-yale-endowment-value-272-billion

[v] http://www.pionline.com/article/20151014/ONLINE/151019943/university-of-minnesota-endowment-reports-57-fiscal-year-return

[vi] https://www.strictlybusinesslawblog.com/2017/06/29/the-life-cycle-of-a-private-equity-or-venture-capital-fund/

[vii] https://en.wikipedia.org/wiki/Case%E2%80%93Shiller_index

[viii] according to the National Venture Capital Association website

[ix] https://www.cnbc.com/2017/04/07/you-can-buy-multiple-houses-for-the-cost-of-one-near-google-hq.html

[x] https://www.reuters.com/article/us-intel/intel-to-invest-7-billion-in-u-s-as-recession-deepens-idUSTRE5196WR20090210

April Newsletter

June Newsletter

Demystifying Startup HR

Head of Finance & Fund Administration- Venture Capital Firm (Remote)

Demystifying Startup HR

3 Portfolio Companies Make Inc. 5000 + Quicklly & Instacart Expand

iraLogix closes $22M + Branch expands with Uber

iraLogix closes $22M Series C

Flywheel lands Gates Foundation grant

Venture Capital Analyst

Orazio Buzza, Founder and CEO of Fooda – on Episode 13, “Execution is King”

$40M Fund II Raised!

Eric Martell, Founder of Pear Commerce: Episode 13, Execution is King

Great North Ventures Raises $40 Million Fund II

Investment Thesis: Fund II Strategy

Investment Theme: Community-Driven Applications

Investment Theme: Digital Transformation Through AI

Investment Theme: Solving Labor Problems

Trends in the Gig Economy + Work in the Metaverse

Portfolio raises $125M + talking fundraising with Branch CEO

Omnia Fishing closes $4M round, joins Great North portfolio!

Atif Siddiqi, Founder/CEO of Branch: Episode 11, Execution is King

Michael Martocci, CEO and Founder of SwagUp: Episode 10, Execution is King

Yardstik new to portfolio, closes $8M Series A

First venture studio startup comes out of stealth!

Insights for founders from a data guru, + FactoryFix raises a Series A!

Una Fox: Episode 9, Execution is King

Start With a Mobile App, Not a Website

2ndKitchen acquired by SoftBank-backed REEF + advice from an early Googler

Joe Sriver, 4giving: Episode 8, Execution is King

2ndKitchen Acquired by REEF

Venture studio startup jobs + advice for founders from founders

Best Advice from the Great North Annual Event: Episode 7, Execution is King

Newsletter: Do you fit our investing themes?

Jonathan Treble, PrintWithMe: Episode 6, Execution is King

Anna Mason, Revolution: Episode 5, Execution is King

Mynul Khan, FieldNation: Episode 4, Execution is King

Nick Moran, New Stack Ventures: Episode 3, Execution is King

Molly Pyle, Center on Rural Innovation (CORI): Episode 2, Execution is King

Justin Kaufenberg, Rally Ventures: Execution is King Episode 1

Newsletter: “Podcast Launched: Execution is King!”

“Execution is King” – the Great North Ventures Podcast

Newsletter: Fund II is open for business!

Unlocking the Potential of Anonymized Commercial Real Estate (CRE) Data

Fund II is open for Business!

Mike Schulte Promoted to Venture Partner

New Name + New Venture Studio

Great North Launches Startup Studio

We Don’t Need No [full-time MBA] Education

How the University of Minnesota is Embracing Startup Culture

Top Stories of 2020, iraLogix, and LaunchMN Calls for Mentors

Building Capacity for Innovation

Seizing Opportunity in a Recession, Allergy Amulet, and Twin Cities Startup Week

Recessionary times, a record-setting IPO, and Minnesota’s Resilient Startups

Minnesota's Resilient Startups

July 4th, Equitable American Dream-ing, and Robots Diagnosing COVID

Jumpstart, the Startup School, and Branch Wins a Webby!

COVID-19 Trends, the Great North response, and our Founders Survey

Giving in the Time of Coronavirus

COVID-19 Resources for Startups, State-by-State

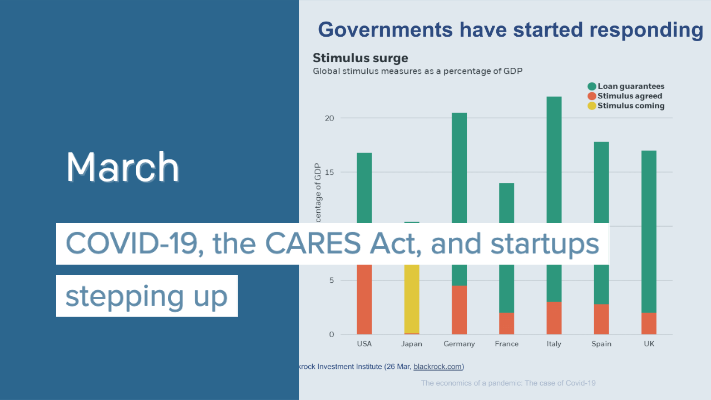

COVID-19, the CARES Act, and startups stepping up

New Business Preservation Act

Digital Future Boardroom, PartySlate, and The Lean Startup School

Great North Labs’s Startup Summit 2020

Great North Labs's Startup Summit 2020

World Economic Forum, NoiseAware, and the Startup School reboot

Great North Labs at the World Economic Forum 2020 in Davos

Top 5 Stories of 2019

Taking the Founders Pledge, Inhabitr, and gBETA Pitch Night

Founders Pledge: Support the Organizations that Support You

BETA Showcase, Greater MN, and Launch MN comes to St. Cloud

7 Places to Spot Us at Startup Week

The Greater MN Meetup, Parallax, and Exponential Medicine

Greater MN at the big show, Neela Mollgaard heads Launch MN, and Misty’s roadtrip.

Talking VC, tech kids, and Forge North’s Horizon

June: Great North Labs’s first fund raised!

May: Innovation Ecosystems, SingularityU Kickoff, and PrintWithMe

April: Minnebar Recap, ZenLord Pro, and Supporting Entrepreneurs

MinneBar 14 Recap

Dispatch and 2ndKitchen claim Tech Madness titles

Minnesota Innovation Collaborative

March: Minnebar, Hockey + Hustlers, and Innovation Workshops

Great North Labs at CES

Dec.-Jan.: Top Posts from 2018, pepr, Glowe, and Misty Robotics

Carried Interest: Top Posts from 2018

Oct.-Nov.: Singularity University, Exponential Tech, and the State of Innovation

Digital Transformation Summit, July 25th in Minneapolis

June: Silicon Lakes, FactoryFix, and the Digital Transformation Summit

Putting the “Silicon” in Silicon Lakes

Digital Manufacturing and Logistics

May: Team Genius, IoT, and the Future of Everything

IoT 3.0

Healthcare Innovation

March: Exponential Tech, the “Goldilocks Zone”, and Minnebar 13

February: Team Expansion, Dispatch, and Startup School Events

Great North Labs Newsletter – December 2017

A Letter To My Younger Self

Great North Labs Newsletter

Great North Labs Featured on Tech.mn

Great North Labs Featured in St Cloud Times

Great North Labs – Featured on BizJournals.com