As a tech founder and investor, I have spent a lot of time thinking about why some startups scale and why others fail. You have to when your livelihood is riding on whether or not you can execute. And when you’re putting other peoples’ money on the line, knowing what to do and being able to do it isn’t enough, but you have to be able to explain your decisions and actions.

When I made enough money as a founder to start angel investing, I was overly focused on the idea and strategy. Why? The business I had founded with my twin brother Ryan Weber was successful in terms of financial returns, but it lacked defensibility. In my opinion, that’s what prohibited our business from scaling to an even greater outcome- we didn’t have a great idea or strategy.

Learning from this lesson from my own business, I compensated by investing in founders who had a clever idea and a good strategy. Sometimes it felt like I was just investing in a nice pitch deck. Many of these teams just could not execute, and over time, they’d fail.

You can be a brilliant founder, with a clever idea and a good strategy, and still fail. It happens all the time. If you can’t attract customers, build a team, and set and achieve goals, you’re sunk.

As a VC, I’ve had to synthesize everything I’ve learned about operating and investing into a scalable, repeatable process- to turn these lessons into actionable guidance for conducting diligence. Founders who work towards these things increase their chances of reaching an exit, and investors who look for these things increase their chances of generating a return.

These are the top 5 signs a startup will succeed.

1) The startup has founders with great soft skills. Having a great idea or writing some really kickass code isn’t enough to scale a big business. Soft skills are even more important than tech skills or industry experience. A founder/CEO’s job includes sales, recruiting top talent, management, etc. All of these are soft skills.

2) The startup has a culture of accountability, and is focused on key growth metrics. Creating a metric driven, accountable culture is challenging. It is easier to do with a 4-person startup than a large-scale growth business so it is a critically important early piece.

3) The startup is good at new product development. Teams that are good at product development are analytical and creative. They run experiments before building a complete product which enables them to avoid focusing on building the wrong product with the wrong features.

4) The startup is focused on finding and perfecting one scalable customer acquisition channel. Experimenting is expected in the very early going, but eventually you need to bet on the one channel that can get you to scale. It could be digital media-focused customer acquisition, a referral program, or viral social strategy, anything that creates compounding returns. You need to be world-class at whatever your dominant channel is to succeed. For most of the best startups, growth is designed into the product or some other kind of clever growth hack is utilized. Look at Airbnb’s famous spamming of Craigslist (Airbnb Growth Study (benchhacks.com)) or DropBox’s famous early referral incentives. This is the scrappy team, focused on the right things, that has found the right product, and a way to scale.

5) The startup has an adaptable, entrepreneurial team. Early-stage is not the time for a team fixated on management systems. The time for investing more heavily in management systems is when your startup approaches 20–50 employees or more. In the beginning, you need a team with entrepreneurial skills, including customer empathy, product engineering strength, and go-to-market strength.

For former founders-turned-investors like myself, we need to be particularly aware of not being overly attracted to clever ideas in big markets, but instead focus on identifying the teams that can find their North Star to take them from point A to point B so the startup has an opportunity to start compounding. Execution is everything.

Healthcare Today

Some of the smartest minds work in healthcare, life sciences and biopharma. Yet the healthcare sector struggles to bring innovation into its ecosystem. The pace of innovation adoption has been much greater in other sectors, including in communication (Facebook, Skype), learning (Google, YouTube, Coursera), shopping (Amazon), personal finance (PayPal), and entertainment (Netflix).

This is not because of a lack of innovation in the pipeline. Healthcare sector innovators are hard at work on drugs and therapeutics, devices, and operational aspects of healthcare delivery. Breakthroughs have come in genomics-based precision drugs, machine-learning-based disease detection, EMRs, payment systems, patient adherence and education tools. In healthcare, the innovation tends to be evidence-based, with scientific papers that quantify results from well-designed experiments, and a highly-skilled academic research ecosystem at their source. That aspect is unique in the healthcare sector, and the sector has other ecosystem attributes not seen in other sectors. It’s this unique ecosystem that makes market insertion, growth and adoption at scale more complex, requiring specific insight and enablement.

The Upper Midwest has substantial healthcare anchors to promote a thriving ecosystem of clinical innovation and practice. Examples include the leading research, teaching and clinical centers of the Mayo Clinic and University of Minnesota; hospital systems like Minnesota Health System and CentraCare; device manufacturer Medtronic; software companies like Epic; payers such as United Healthcare; and the processors Optum and United. There are also hundreds of strong, related entities across the region. Healthcare investment is shifting from traditional hotspots like Boston, Houston, and Raleigh-Durham to Silicon Valley, and while the global ecosystem catches up, there is an opportunity to take advantage of this transition to strengthen the ecosystem in the Upper Midwest.

Strong healthcare research leads to breakthrough ideas which require mentorship and incubation to grow. Leading research institutions can organize ecosystem support, such as how the University of Minnesota encourages mentorship through their Venture Center’s Business Advisory Group which brings together entrepreneurs, funds (including Great North Capital Fund), and industry leaders to drive the successful commercialization of its academic research. This is big business, and the U of MN now generates roughly $1B per year from such efforts (two-thirds life sciences and one-third software/IT).

Geographic and industry-themed startup accelerators have also begun to proliferate in the region. Startup accelerators support early-stage, growth-driven companies through education, mentorship, and financing for a fixed period of time, among an admitted cohort of companies. The multi-city startup accelerator, Gener8tor, is managing a new Twin Cities med-tech accelerator backed by Boston Scientific, the University of Minnesota, and the Mayo Clinic. Venture studios and incubators are other forms of early-stage support available in the region. Minneapolis-based Invenshure has successfully launched multiple healthcare startups.

The region’s healthcare system is also significant on the demand side. For example, the cost drivers of healthcare in Minnesota reflect those in the US at large. Yet, while challenges in patient care are also similar to those of other regions, Minnesota’s efficiency is better. Healthcare spending accounts for over 16% of the US economy but is only about 13% of the Minnesota economy. So not only are Minnesota-based insights relevant, they are valuable. Innovations can be developed and piloted in Minnesota, then applied in other states. Startups developed here can be scaled nationally and, with adaptation, internationally.

Figure 1: Health Care Cost Drivers: Spending and Shares of Growth by Service, 2011 to 2013.

(Source: Minnesota Department of Health).

Change is Accelerating

Each decade brings its own set of innovations that transform industries. The healthcare industry will undergo vast changes in the next 10-20 years. The growing spate of investments and partnerships among tech innovators is signaling an increasing rate of change in this sector. The most visible examples of these innovators include Amazon, Apple, Google, Qualcomm, and Walmart. Google Ventures alone did 27 healthcare deals in 2017, up from 9 in 2013.

These companies you wouldn’t normally think of as bastions of healthcare innovation, yet they are all allocating large talent pools and budgets in the industry. Until Tesla, who would have thought that the next innovation in cars would come from Silicon Valley? More than their balance sheets, the noteworthy attributes of these companies are their culture of observing ecosystems, and their practice of inserting innovation in a stepwise and sustained manner to upend markets.

When you combine such entities with those like Berkshire Hathaway and Goldman Sachs (both of whom are partnering with Amazon in healthcare), and the financial and corporate venture groups that work with them, a disruptive landscape begins to take shape in which other innovators and incumbents alike can find new opportunities. For innovators, it means aligning their innovations with insertion points with high economic value and low resistance. For incumbents, at minimum, it means awareness and being prepared; more proactively, it means proactive engagement with capital (e.g., investments through VC firms), pilots, and adoption. For example, the Mayo Clinic has partnered with Google on leveraging its Knowledge Graph smart search algorithm for patient education, and Optum’s venture arm (based in Boston and Silicon Valley) has allocated $250M to venture investments

The range of innovations in the pipeline is equally stunning. Early examples include smartphones coupled with wearables for clinical-grade data. Today’s pipeline includes voice assistants (trained Alexa-like products) for health-related questions, machine vision for detecting physical anomalies (in skin, bones, retinae, or genes) or even bacteria in food. There are AI and visualization-enabled robotic surgery tools for doctors (e.g., Verb Surgical); machine learning in patient-specific onset detection for things like allergies and COPD; big data in early cancer detection (e.g., Freenome) and other diseases like multiple sclerosis, Parkinson’s and autism. The Mayo Clinic and AliveCor have shown that an AI can be trained to identify people at risk for arrhythmia and sudden cardiac arrest despite normal EKG results. There is also analytics-optimized underwriting for individuals and small businesses (e.g., Oscar), Medicaid (Clover) and self-insured populations (Collective Health).

Enabling the Innovation

Applying capital to create, enable and grow innovation platforms, align disruption with practical value in startups, and engage institutions for initial adoption, deployment at scale, and sustained growth requires a deep understanding of the ecosystem and cross-disciplinary skills to navigate it. This is especially true in healthcare given the ecosystem’s unique attributes and complexity, the importance of human health, government regulation, and the depth of incumbency among some players.

Startups benefit from focused enablement of resources including mentors, partners, lab space, hardware/software development expertise, and communication and data analysis platforms. Healthcare enterprises benefit from investment partners who understand their service goals and the need to balance innovation within financial constraints and with operational realities such as the need for patient privacy and the limitations of government regulations.

At Great North Labs, we focus on bringing such forces together to apply capital and expertise effectively and efficiently. We study ecosystems and leverage experts as advisors. We bring people together at events and entrepreneur training, through referrals, and with investment, mentorship and thought leadership by our team. We apply our capital and resources locally, with a deep connection to innovation hubs nationally, and with the goal of scaling globally.

April Newsletter

June Newsletter

Demystifying Startup HR

Head of Finance & Fund Administration- Venture Capital Firm (Remote)

Demystifying Startup HR

3 Portfolio Companies Make Inc. 5000 + Quicklly & Instacart Expand

iraLogix closes $22M + Branch expands with Uber

iraLogix closes $22M Series C

Flywheel lands Gates Foundation grant

Venture Capital Analyst

Orazio Buzza, Founder and CEO of Fooda – on Episode 13, “Execution is King”

$40M Fund II Raised!

Eric Martell, Founder of Pear Commerce: Episode 13, Execution is King

Great North Ventures Raises $40 Million Fund II

Investment Thesis: Fund II Strategy

Investment Theme: Community-Driven Applications

Investment Theme: Digital Transformation Through AI

Investment Theme: Solving Labor Problems

Trends in the Gig Economy + Work in the Metaverse

Portfolio raises $125M + talking fundraising with Branch CEO

Omnia Fishing closes $4M round, joins Great North portfolio!

Atif Siddiqi, Founder/CEO of Branch: Episode 11, Execution is King

Michael Martocci, CEO and Founder of SwagUp: Episode 10, Execution is King

Yardstik new to portfolio, closes $8M Series A

First venture studio startup comes out of stealth!

Insights for founders from a data guru, + FactoryFix raises a Series A!

Una Fox: Episode 9, Execution is King

Start With a Mobile App, Not a Website

2ndKitchen acquired by SoftBank-backed REEF + advice from an early Googler

Joe Sriver, 4giving: Episode 8, Execution is King

2ndKitchen Acquired by REEF

Venture studio startup jobs + advice for founders from founders

Best Advice from the Great North Annual Event: Episode 7, Execution is King

Newsletter: Do you fit our investing themes?

Jonathan Treble, PrintWithMe: Episode 6, Execution is King

Anna Mason, Revolution: Episode 5, Execution is King

Mynul Khan, FieldNation: Episode 4, Execution is King

Nick Moran, New Stack Ventures: Episode 3, Execution is King

Molly Pyle, Center on Rural Innovation (CORI): Episode 2, Execution is King

Justin Kaufenberg, Rally Ventures: Execution is King Episode 1

Newsletter: “Podcast Launched: Execution is King!”

“Execution is King” – the Great North Ventures Podcast

Newsletter: Fund II is open for business!

Unlocking the Potential of Anonymized Commercial Real Estate (CRE) Data

Fund II is open for Business!

Mike Schulte Promoted to Venture Partner

New Name + New Venture Studio

Great North Launches Startup Studio

We Don’t Need No [full-time MBA] Education

How the University of Minnesota is Embracing Startup Culture

Top Stories of 2020, iraLogix, and LaunchMN Calls for Mentors

Building Capacity for Innovation

Seizing Opportunity in a Recession, Allergy Amulet, and Twin Cities Startup Week

Recessionary times, a record-setting IPO, and Minnesota’s Resilient Startups

Minnesota's Resilient Startups

July 4th, Equitable American Dream-ing, and Robots Diagnosing COVID

Jumpstart, the Startup School, and Branch Wins a Webby!

COVID-19 Trends, the Great North response, and our Founders Survey

Giving in the Time of Coronavirus

COVID-19 Resources for Startups, State-by-State

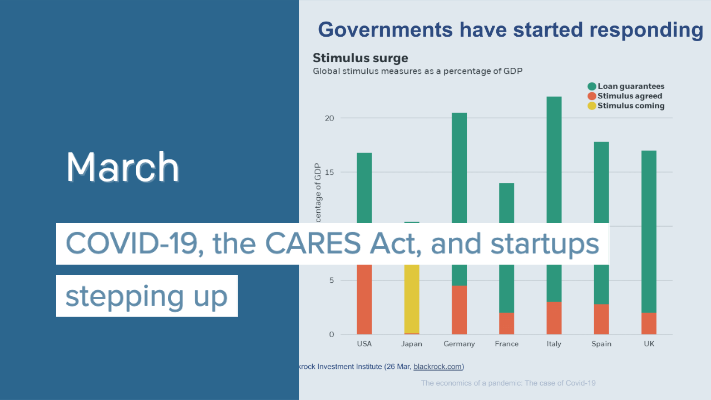

COVID-19, the CARES Act, and startups stepping up

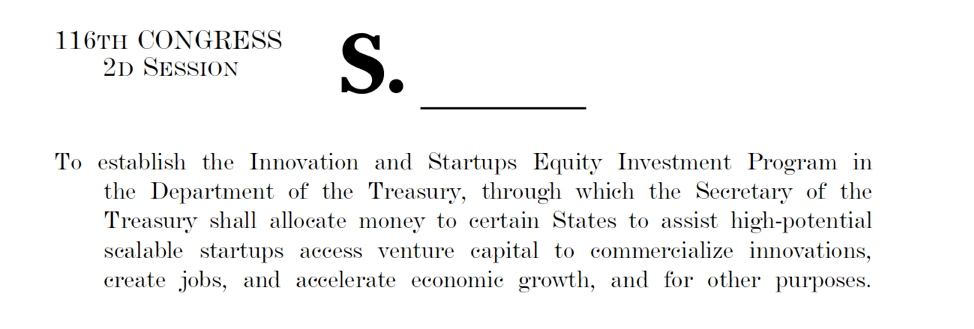

New Business Preservation Act

Digital Future Boardroom, PartySlate, and The Lean Startup School

Great North Labs’s Startup Summit 2020

Great North Labs's Startup Summit 2020

World Economic Forum, NoiseAware, and the Startup School reboot

Great North Labs at the World Economic Forum 2020 in Davos

Top 5 Stories of 2019

Taking the Founders Pledge, Inhabitr, and gBETA Pitch Night

Founders Pledge: Support the Organizations that Support You

BETA Showcase, Greater MN, and Launch MN comes to St. Cloud

7 Places to Spot Us at Startup Week

The Greater MN Meetup, Parallax, and Exponential Medicine

Greater MN at the big show, Neela Mollgaard heads Launch MN, and Misty’s roadtrip.

Talking VC, tech kids, and Forge North’s Horizon

June: Great North Labs’s first fund raised!

May: Innovation Ecosystems, SingularityU Kickoff, and PrintWithMe

April: Minnebar Recap, ZenLord Pro, and Supporting Entrepreneurs

MinneBar 14 Recap

Dispatch and 2ndKitchen claim Tech Madness titles

Minnesota Innovation Collaborative

March: Minnebar, Hockey + Hustlers, and Innovation Workshops

Great North Labs at CES

Dec.-Jan.: Top Posts from 2018, pepr, Glowe, and Misty Robotics

Carried Interest: Top Posts from 2018

Oct.-Nov.: Singularity University, Exponential Tech, and the State of Innovation

Digital Transformation Summit, July 25th in Minneapolis

June: Silicon Lakes, FactoryFix, and the Digital Transformation Summit

Putting the “Silicon” in Silicon Lakes

Digital Manufacturing and Logistics

May: Team Genius, IoT, and the Future of Everything

IoT 3.0

Healthcare Innovation

March: Exponential Tech, the “Goldilocks Zone”, and Minnebar 13

February: Team Expansion, Dispatch, and Startup School Events

Great North Labs Newsletter – December 2017

A Letter To My Younger Self

Great North Labs Newsletter

Great North Labs Featured on Tech.mn

Great North Labs Featured in St Cloud Times

Great North Labs – Featured on BizJournals.com