Newsletter: Do you fit our investing themes?

Welcome back to the Great North Ventures newsletter! (Sign up here!) This month we have some advice for founders as […]

Welcome back to the Great North Ventures newsletter! (Sign up here!) This month we have some advice for founders as […]

Rob and Josef talk podcasts, and comes clean about his awkward intro to Nick Moran. Nick talks about his path

Commercial real-estate (CRE), a $12 trillion industry, has been slow to use new technologies and data that can boost economic

While there are vaccines on the horizon and a potential further stimulus package, possibly in time for the holiday season,

The world is changing, and a new wave of tech entrepreneurs are shaping the new normal. The tech sector is performing well as

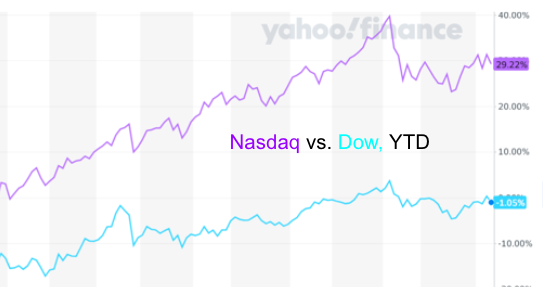

Tech Sector’s Growth has Accelerated It is no secret that during the pandemic, the tech sector is delivering stronger returns

Last month we wrote about the history of local startups that were formed during a recession and went on to

$23.7 Million Raised Great North Labs has closed its first fund with $23.7M in committed capital! This is one of the

More than 8,000 venture-backed companies received a combined $85 billion in funding in 2017, representing the highest annual total since